What does the data show?

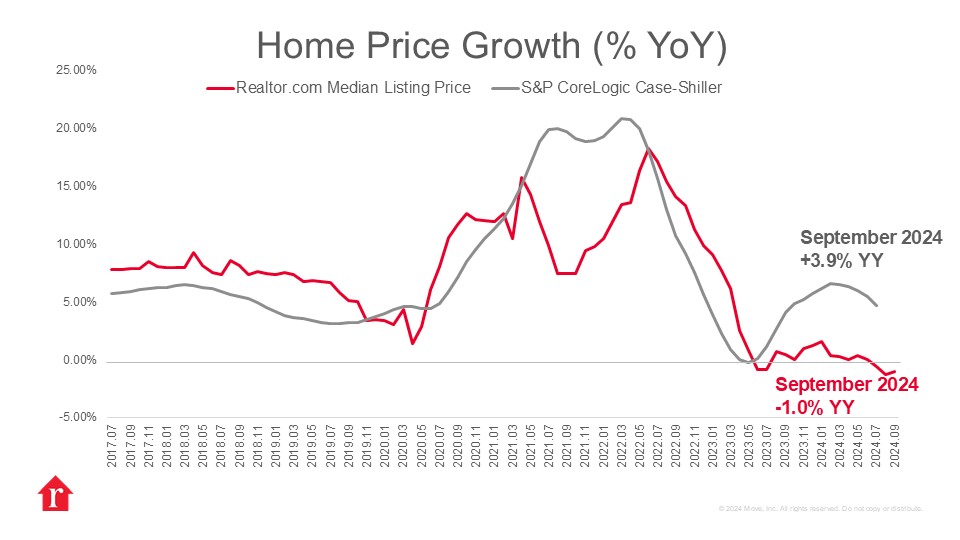

The S&P CoreLogic Case-Shiller Index notched 3.9% higher annually in September, slowing compared with previous months. The 10- and 20-city index saw annual increases of 5.2% and 4.6%, respectively, down from 6% and 5.2% the previous month. This month’s release covers home sales in July, August, and September, a period in which the market continued to tilt in buyers’ favor.

Mortgage rates reached a recent low of 6.08% at the end of September, closing out a roughly five-month period of easing mortgage rates. Eager buyers took advantage of this temporary respite, which resulted in a 3.4% bump in existing-home sales in October. However, mortgage rates started to climb once again, reaching as high as 6.84% last week, which will likely hurt buyer demand and home sales through the end of the year.

How did trends vary by region?

Regional variation in the housing market means that buyers across the country face significantly different homebuying conditions. Markets in the Midwest and Northeast continue to see substantial demand, while the South and West continue to soften as inventory builds. Similar to last month, New York City (+7.5%), Cleveland (+7.1%), and Chicago (+6.9%) saw the highest price growth, while Denver (+0.2%) saw the slowest.

What is ahead for housing?

Though the housing market is still relatively challenging, the rental market is a favorable alternative as rents continue to ease in much of the country. Rental supply is expected to grow as multifamily units are completed, which could take even more pressure off of rents.

On the for-sale side, home price growth will likely continue to slow as long as buyer demand remains lackluster. Though falling mortgage rates mean more affordable homeownership, an uptick in demand could send prices climbing once again if inventory fails to keep pace. A steady increase in both housing supply and demand will be necessary to maintain market balance.

Note: This article have been indexed to our site. We do not claim legitimacy, ownership or copyright of any of the content above. To see the article at original source Click Here

Apple AirTag

$22.07 (as of February 22, 2025 19:40 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Etekcity Food Kitchen Scale, Digital Grams and Ounces for Weight Loss, Baking, Cooking, Keto and Meal Prep, LCD Display, Medium, 304 Stainless Steel

$13.99 (as of February 22, 2025 20:14 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Libbey Small Glass Prep Bowl 8 Count (Pack of 1), Glass Containers with Lids Keep Leftovers Fresh, Durable Dishwasher Safe Glass Meal Prep Bowls, Glass Bowls Set for Meal Prepping, Snacks

(as of February 22, 2025 19:40 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

EF ECOFLOW Portable Power Station DELTA 2, 1024Wh LiFePO4 (LFP) Battery, 1800W AC/100W USB-C Output, Solar Generator(Solar Panel Optional) for Home Backup Power, Camping & RVs

$449.00 (as of February 22, 2025 19:40 GMT +00:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)